The first half of 2025 revealed a U.S. economy that remains fundamentally resilient despite volatility in growth and policy expectations. A sharp rebound in Q2 GDP, easing inflation, a stable labor market, and moderate equity gains all underscore an investment climate with improving fundamentals and favorable valuations.

We believe investors should stay constructive on risk assets, especially given the alignment of economic momentum and earnings potential heading into H2.

Macro Review: H1 2025

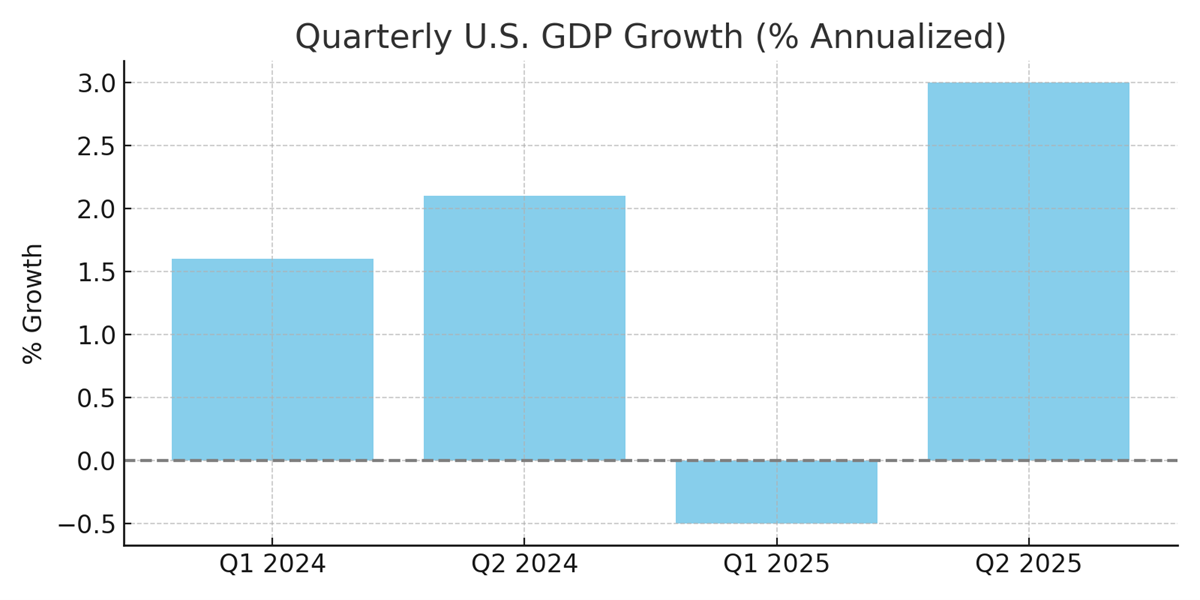

GDP Growth Stabilizing

After a –0.5% annualized contraction in Q1, Q2 delivered a +3.0% rebound. This turnaround was driven by:

- A normalization in trade balances

- Robust consumer spending

- Diminished fiscal drag

Labor Market Remains Tight

Despite moderation in hiring—especially into Q3—the unemployment rate remains low, and April saw a surprise upside with +177,000 jobs added. Labor demand is cooling, but not collapsing. Consumers remain well-supported.

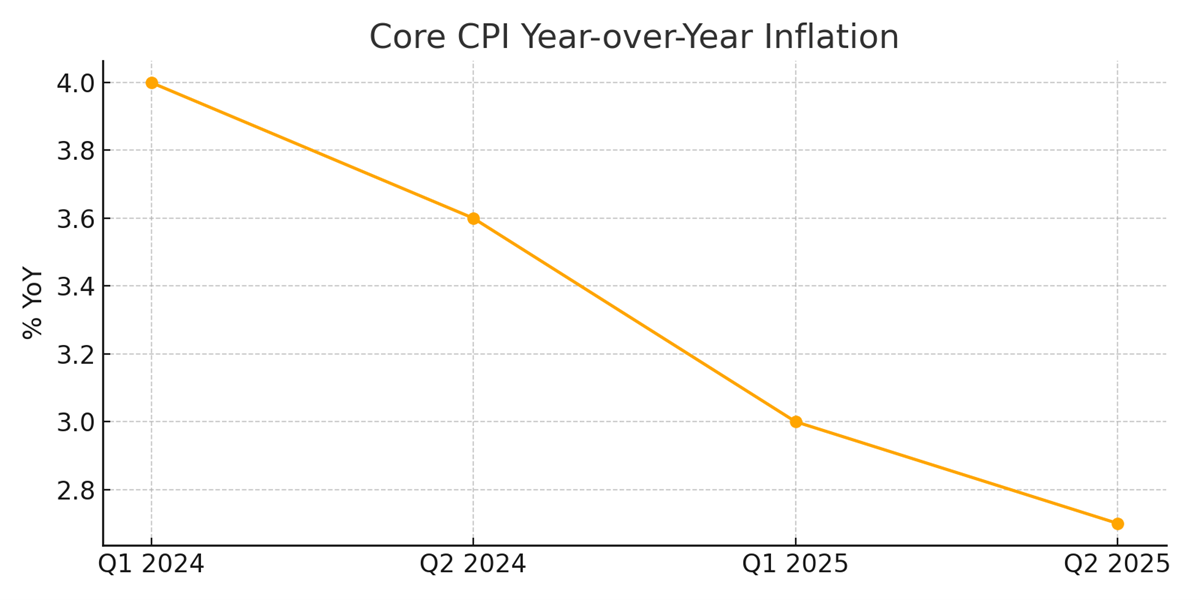

Inflation Cooling

Core CPI fell to 2.7% YoY by June 2025, down from over 4.0% in early 2024. This supports both consumer real incomes and Fed policy flexibility.

Market Overview: H1 2025

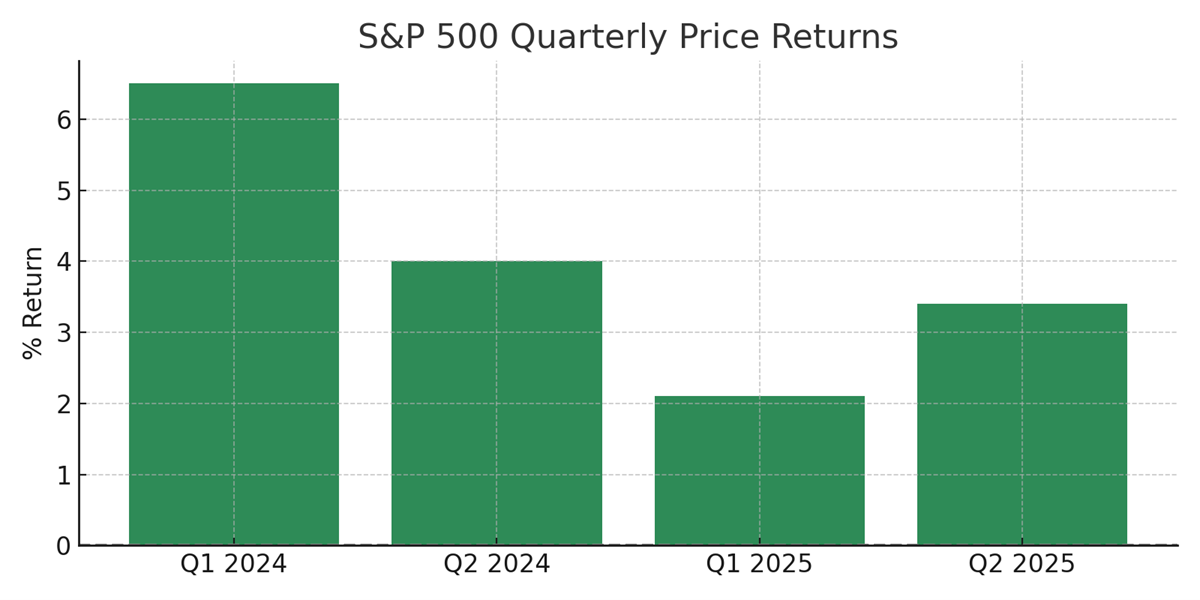

Equity Markets Deliver Despite Uncertainty

The S&P 500 returned +5.5% (price) and about +6.2% (total return) in the first half. This performance came amid earnings stability and resilient economic indicators.

Valuations: Better Entry Points

Forward P/E stands around 22×, holding steady year-over-year. Earnings expectations for 2025 have improved to mid-single digits (5–7%). The market is not overvalued relative to historical norms when adjusted for inflation, growth, and earnings quality.

Sector Performance

Top performing sectors in H1 2025:

- Financials: +19.6%

- Industrials: +12.7%

- Communication Services: +11.1%

- Tech: +8.1%

AI mega-caps accounted for ~40% of S&P gains, but participation has broadened notably across cyclicals.

Currency & Global Positioning

Despite a –11% move lower YTD, the U.S. dollar is supported by:

- A rare trade surplus in June

- Tariff uncertainty easing via trade deals

- Yield differentials still favoring U.S. Treasuries

Looking Ahead: Strategy for H2 2025

Expectations:

- Real GDP growth to trend 2.0–2.5% annualized

- Continued disinflation toward Fed’s 2% target

- Fed cuts possible by Q4 if inflation progress persists

- Earnings growth to re-accelerate as cost pressures ease

Sector Themes for Allocation:

- Financials: Leveraged to rates and GDP rebound

- Industrials & Materials: Benefit from global capex cycles

- Communication & Tech: AI tailwinds with selective valuation

- U.S. Dollar-Hedged International: Especially as Fed holds

Bottom Line

Midway through 2025, the U.S. economy continues to defy pessimism. The data shows a story of resilient growth, easing inflation, stable jobs, and improving corporate fundamentals. Market valuations remain reasonable—and the dollar may be at a turning point. For forward-looking investors, the setup into H2 is increasingly attractive.